.jpg)

In June’s TaaS magazine the drive towards connected vehicles and services is more urgent than ever before. As Graham Gordon from LexisNexis Risk Solutions highlights in his article:

“There are already an estimated 20 million cars in the US with connectivity capability, 11 million between UK, Germany, France, Italy and Spain and this volume is set to grow with 100% of new cars expected to have connectivity by 2025[i]. The growth in connected car data is on a steep trajectory.”

This data needs to be accurate, so testing in a virtual environment saves both time and cost as discussed in Claytex's article 'The importance of accurate sensor models for the Virtual testing of Autonomous Vehicle'.

Mobility-as-a-service is gaining more popularity as the way forward but as Boyd Cohen & Phil Williams from Iomob discusses, there are thousands of mobility providers, but they don’t connect together well, if at all. Maybe we need to look at On-Demand Mobility Service Design as Raphael Gindrat from Bestmile discusses. But with all of this there are risks, so who is going to take this risk? But then is 'MaaS, a river or a cheese?' one of the stranger questions to be asked, but asked by Markus Aarflot is a Business Developer at UbiGo.

Lightyear has introduced its first long-range solar car. The prototype was presented to investors, customers, partners and press at dawn in Katwijk, the Netherlands.

“This moment represents a new era of driving,” said Lex Hoefsloot, CEO and Co-Founder of Lightyear. “Climate change is such a frightening development that it's almost paralysing. We decided to do the opposite; as engineers, we believed we could do something. Lightyear One represents an opportunity to change mobility for the better.”

“Since new technology has a high unit cost, we have to start in an exclusive market. The next models we plan to develop will have a significantly lower purchase price. In addition, future models will be provided to autonomous and shared car fleets, so the purchase price can be divided amongst a large group of users. Combined with the low operating costs of the vehicle, we aim to provide premium mobility for a low price per kilometre,” Hoefsloot added.

Lightyear One will get to a range of 725 km on the WLTP cycle. The company also guarantees at least 400km in winter, at highway speeds and with heating on. Mostly, range will be between 500 and 800 kilometres.

The efficiency of Lightyear One means that it's possible to get more charging performance from any charging outlet in less time. Through fast charging, one can charge up to 570km worth of energy within an hour and with a simple 230V outlet, it's even possible to charge up to 350km worth of energy overnight.

Lightyear One is propelled by four independently driven wheels. In addition to lowering the weight and improving control, it means that no energy is lost in transit from the motor to the wheel. Lightyear One offers drivers unique control.

The car also has a remarkably low aerodynamic drag, with the best aerodynamic coefficient of any car on the market. This increases the range of the car by decreasing energy consumption.

The roof and hood of Lightyear One comprise of five square metres of integrated solar cells within safety glass so strong that a fully grown adult can walk on them without causing dents. Unlike conventional solar panels, these cells function independently. This means that even if part of the roof or hood is in shadow, the other cells continue to efficiently collect solar energy. In fact, the solar cells provide about 20% more energy than traditional ones.

The solar roof and hood charge up to 12 km/h in the sun. Climate and driving frequency will determine the percentage of mileage this can give. Someone driving the national average of 20,000 km/year in the cloudy Netherlands would get about 40% of their mileage from solar energy. Lightyear One has a solution to accidentally running out of battery. One can drive 15-20km/h on what the solar roof and hood absorb from daylight, getting the vehicle to an outlet with no roadside assistance required. The solar roof and hood are designed to withstand high temperatures when charging, with no loss of efficiency.

BlackBerry Limited announced that its QNX software is now embedded in more than 150 million cars on the road today. This is an increase of 30 million cars since the company reported its automotive footprint in 2018.

BlackBerry, a leader in automotive cybersecurity, has the highest level of automotive certification for functional safety with ISO 26262 ASIL D and decades of experience in powering mission-critical embedded systems in automotive and other industries. Automotive OEMs and Tier 1s use BlackBerry QNX technology in their advanced driver assistance systems, digital instrument clusters, connectivity modules, handsfree systems, and infotainment systems that appear in car brands, including Audi, BMW, Ford, GM, Honda, Hyundai, Jaguar Land Rover, KIA, Maserati, Mercedes-Benz, Porsche, Toyota, and Volkswagen.“

As this milestone proves, BlackBerry's footprint in the automotive industry has never been stronger,” said John Chen, Executive Chairman and CEO, BlackBerry. “The world's leading automakers, Tier 1s, and chip manufacturers continue to seek out BlackBerry's safety-certified and highly-secure software for their next-generation vehicles. Together with our customers we will help to ensure that the future of mobility is safe, secure and built on trust.”

BlackBerry engaged with research and industry analyst firm, Strategy Analytics to verify the volume of QNX deployments based on the number of QNX products that are shipped in the automotive market and the number of cars that contain QNX products and technology. The vast majority of QNX software products that are integrated and used in automotive ECUs are licensed on a per-unit royalty basis. BlackBerry QNX technology includes QNX Neutrino OS, QNX Platform for ADAS, QNX OS for Safety, QNX CAR Platform for Infotainment, QNX Platform for Digital Cockpits, QNX Hypervisor 2.0 and QNX acoustics middleware.

Fairfax County and Dominion Energy are partnering on an autonomous electric shuttle pilot tentatively planned for the Merrifield area in Fairfax County.

The demonstration project moved a step closer to implementation with the award of a grant from the Virginia Department of Rail and Public Transportation (DRPT) for the execution of the pilot.

The Virginia Commonwealth Transportation Board approved the $250,000 grant for Fairfax County, making this pilot the first state-funded autonomous public transportation demonstration project in Virginia. The pilot would also be one of the first tests of driverless technology in public transportation in Virginia. Fairfax County will provide a $50,000 local match to the DRPT grant.

The goal of the pilot is for Fairfax County and Dominion Energy to learn about the various aspects of deploying autonomous vehicles as part of a large public transportation system. Fairfax County aims to be at the forefront of innovation by testing this smart technology for economic and environmental benefits, operational efficiencies and as a first and last mile travel option connecting people from Metrorail stations to employment, activity centers and residential communities.

Dominion Energy is committed to being a driver of change and supporting innovative projects that will reduce carbon emissions and help customers do the same. Autonomous and electric vehicle technology will play a major role in a lower-emissions transportation future in the Commonwealth of Virginia and across the nation.

The Fairfax County Board of Supervisors will consider a formal partnership agreement between Fairfax County and Dominion Energy on June 25, 2019. As part of the proposed partnership, Dominion Energy would lease or buy the vehicle for this pilot and Fairfax County would oversee the operations.DRPT is committed to ensuring Virginia is on the forefront of new mobility innovations, including the deployment of autonomous transit. DRPT is providing demonstration funds to offset the cost of operations and is evaluating how shuttles can provide critical first and last mile connections to transit.

Safety will be key to the successful implementation of the pilot and the project is subject to safety reviews by the Virginia Department of Transportation (VDOT) and the National Highway Traffic Safety Administration (NHTSA). The shuttles will undergo extensive testing before passenger service can begin and a safety steward will be on board to monitor operations.

A zero-emission E-truck developed with ABB technology was seen on the streets of Swiss capital Bern for the first time, paving the way for sustainable urban logistic solutions.

The E- truck has been developed in collaboration with ABB's pilot truck manufacturer partner E-Force One, with the aim of having an all-electric ABB delivery fleet in Switzerland by the end of 2022.The truck, which delivered an ABB Formula E ‘Gen2' racecar to a launch event for the ABB FIA Formula E race in Bern, incorporates an electric motor, inverter, traction auxiliary and battery systems from ABB. The batteries are charged with ABB Terra 54 fast chargers and provide enough power for a range of up to 300km.

The first two trucks will be garaged at ABB's power electronics factory in Turgi, northern Switzerland. After a test phase of several months ABB's current fleet of eleven diesel vehicles will be superseded over the next three years by a single-operator fleet of E-trucks. The change will save an estimated 400 tonnes of CO2 emissions every year, for no extra operating cost.Morten Wierod, President of ABB's Motion business, said, “The E-truck was a prime example of ABB's commitment to technology innovation. The new powertrain for trucks is a significant piece of e-mobility technology for heavy vehicles. It shows our advancement in developing technologies that are more energy efficient with a lower-carbon output. We will also be using the E-truck in our own daily business operations.”

ABB will be the first company in Switzerland to trial fully electric truck deliveries and they will benefit during the testing period from the established fixed routes between ABB facilities. The longest scheduled distance for delivery within Switzerland is 235km - well within the 300km range of the EF26 three-axle vehicles selected for the trial. A range of up to 500km would be possible with the largest available battery fitted.

The prototype 25-tonne vehicles will be fitted with a 310kWh battery, charged for six hours overnight at the Turgi base. The 360kW ABB motors produce 2700Nm of torque, making the e-truck capable of hauling a 12-tonne load with a standard trailer. Their maximum speed is limited to 85km/h, with negligible road noise apart from that generated by the tyres.Marcel Schütz, ABB Head of Transport & Trade Switzerland, added: “The E-trucks will cover approximately the same distance every day, so they can be designed explicitly to fit ABB's needs. This is the perfect logistics solution for our needs.”

Energy supplied to the charging stations at the trucks' Turgi base would be sustainably sourced, also thanks to solar panels and inverters already installed at the factory. Successful integration of a full E-truck fleet into ABB's logistics operations would significantly enhance the company's global Mission to Zero commitment, which is aiming to build a carbon-neutral and energy self-sufficient ecosystem for industry, homes and cities.

In part one of Waiting for the Robots, I posed some questions about how cities and regulators might change to make the deployment of autonomous cars easier. In part two, I examine the autonomous vehicles that may come sooner than fully autonomous cars.

Among experts, there’s a very wide range of opinion about when driverless cars will be “ready” (leaving aside what that even means precisely), and as big a gap about how long they will take to become widespread. But alongside the prestigious race to launch the self-driving car, there’s a very important “warm-up” race - to deploy and commercialise other autonomous and semi-autonomous vehicles, not necessarily designed to carry individual people.

The primary focus of these typically smaller vehicles is on the delivery of items to consumers. From food to essential supplies, several startups and established companies are unleashing myriad robots onto our roads, sidewalks and even skies as beach-head devices flying the flag for autonomy ahead of their better-known cousin, the self-driving car.

It’s easy to see why delivery vehicles comprise an attractive category - there’s far more design flexibility than with cars, far less regulation and a lower threshold for consumer acceptance compared to replacing their beloved and trusted means of conveyance. A 20kg (44lbs) robot trundling along the sidewalk at a non-threatening 6kmph (4mph) is much less controversial than a 2 ton car without a human at the wheel, however poorly some humans drive.

With sidewalk bots like those from Starship and Kiwi having completed over 30,000 deliveries each, of payloads up to 10kg (22lbs), and trials underway with hundreds of the little rovers in multiple cities, these may be among the first autonomous vehicles often encountered by the public at large. Costing substantially less than most delivery vehicles and operating at a fraction of the cost of a human-piloted car, these bots enable free, or virtually free, deliveries. Fully electric, their environmental footprint is as proportionately small as their physical size is to ICE cars typically used for deliveries. Although Kiwi and Starship are the most common providers so far, there are plenty of others in the game - FedEx have also announced experiments with a delivery bot that can even climb steps to a porch, while Amazon have recently trialed their Scout device in Washington.

Self-driving vehicles and sidewalk robots could slash last-mile delivery costs in cities by as much as 40 percent and could make up 85% of last mile deliveries.

But delivery bots are not without their opponents. Questions over their presence on sidewalks, their interactions with, for example, wheelchairs on a narrow pathway and vulnerability to anti-social behavior mean not everyone is welcoming them - while Virginia and Idaho have rolled out the welcome mat (or more exactly welcome legislation), there’s a ban in most areas of San Francisco.

Larger capacity vehicles clearly don’t belong on sidewalks, but also may not need to mix with highway traffic. One interesting interim solution is the Nuro - this autonomous delivery vehicle is designed for suburban use and only about half the width of a compact car - operating on the road but at slow speeds of only 40 kmph (25 mph). Currently being tested in Texas, the R1 can carry loads up to 100kg (220 lbs) - so much more than sidewalk bots - and the success of its initial operations has seen investments in the startup of nearly $1 billion.

Drones have quickly got themselves a tarnished reputation, with widely reported disruptions of airports and hastily implemented ownership registration schemes to control irresponsible use. But some of the world’s largest companies are eagerly pursuing airspace solutions to deliveries. On a recent trip to Silicon Valley, I spent some time chatting to the folks at Wing, the Alphabet division developing autonomous aircraft for consumer deliveries.

Already live in trials in Canberra (70,000 test flights) and shortly to commence in Helsinki, these autonomous aircraft fly at up to 120km/h (75mph) before hovering at 7m (23ft) to lower their 1.5kg (3 lbs) payload to the customer below. Just last week (June 4th), Amazon announced its near-final aircraft during the ReMars event, which they say will be ready for use within “months”.

These all-electric drones have a fairly obvious benefit for fast deliveries but will raise many privacy, safety and noise pollution concerns from people under the flight paths.

Away from the world of logistics and last mile delivery, Shuttles comprise another area of autonomous transport showing real early traction. Typically operating at low speeds on partially protected routes, they offer a non-threatening introduction to autonomous transport. Seating up to 10 people, they are ideal for use in large factories, campuses or even to link to suburban transit stations.

There are plenty of other examples of autonomous technology slowly moving out from the labs into the outside world. But much of it is avoiding direct interactions with unpredictable humans for now, while learning to navigate simpler worlds. But if you look hard enough, you can find autonomous sweepers out early on the streets of Disneyland Shanghai, or indoors in Seattle-Tacoma airport and at some Walmart stores. Swedish startup Einride has just announced trials of a freight solution that can haul 26 tones.

Einride freight trial with a Driverless Cab

So it seems we’ll see myriad other autonomous and semi-autonomous vehicles before self-driving cars become commonplace. As autonomy continues to advance from these simpler use cases, I believe we’ll see it expand cautiously but continuously through new use cases. I suspect it won’t be long until we see lower-risk deployments - how about night-time rebalancing (moving the cars to areas of higher demand) of shared cars such as Zipcar or RideNow? The less crowded roads with less vulnerable road users (cyclists/pedestrians) about would make for a more forgiving environment than day-time operations, while empty cars could always err on the side of caution without worrying about passengers.

There are fascinating changes ahead as autonomy takes hold - on roads, sidewalks and in the skies above us before we get to fully autonomous cars. In a way, it feels like these other examples of autonomous technologies are like an advance party, testing consumer reaction and paving the way for their more disruptive successors to come. What if consumers react negatively to these early encounters with autonomy? Could a backlash delay driverless car, even if the technological and regulatory challenges are solved? Even if they’re not aware of their trailblazing role, these robots are a vital barometer of public opinion preparing us for self-driving cars.

Mobility, at its simplest, is about getting people from A to B in the most convenient way possible. While big players in the field have been making the journey smart, electric or autonomous, what3words has focused on how we talk about A and B, exactly, how making them as precise and simple as possible makes for a better user experience, and how that is helping usher in the future of mobility.

A and B are locations. A starting point and a destination, usually communicated to another person or a machine via a street address. The problem is, street addresses were developed to make delivering mail easy in places that were never expected to grow as much as they did. They are unreliable and unsuitable for the ways we move and navigate today.

Addresses are slowing us down

We’ve all had our gripe, at one point or another, with addresses and maps. Pins drop in the centre of buildings with no indication of where the actual entrance is. Postcodes cover large areas. Duplicate street names cause mistakes. Satnavs tell us we’ve arrived when we haven't really. New builds don’t appear on maps even though people have started living there and are using their new addresses every day.

Then, there are all the places that have no address like food trucks, beaches, and fields, and all the developing countries and rural areas around the world that lack a formalised addressing system.

-isbbgh.jpg)

Finally, when it comes to navigation, satnav interfaces are clunky and frustrating, and while voice has become a common way to input commands into a phone or home voice assistant, addresses are particularly difficult to enter by voice correctly.

what3words solves these issues.

A future-proof addressing system

what3words has divided the world into 3m squares and given each one a unique 3 word address. For example, ///purist.enjoyable.presides takes you to the front entrance of TaaS 2019.

[The free what3words app helps find, share and navigate to 3 word address]

People can find 3 word addresses where they would normally find location information like guide books, contact pages, and online listings, or they can be shared with them by other people. They can also discover them on the free what3words app or online map.

With 3 dictionary words, they can input a precise destination anywhere in the world, with 3m x 3m accuracy, whether it’s their front door, a remote viewpoint, or a taverna on the beach. When entered into a navigation interface or a ride-hailing platform, a 3 word address is converted to GPS coordinates in the background, providing the machine with a precise destination to navigate to.

what3words is also the only addressing system optimised for speech recognition technology: each address is unique, homophones have been removed, and a smart error detection system helps identify and correct mistakes. The numbers speak for themselves: 3 word addresses are 25% faster to enter by voice than street addresses, and what3words voice drives a 135% increase in address recognition.

[what3words in action in Mercedes-Benz’ MBUX infotainment system]

Improving user experience

The system has been integrated into Mercedes-Benz’s new MBUX infotainment system and is now available in millions of cars in which drivers can now say ‘Hey Mercedes, take me to //grab.venue.glass’ to get directions to, in this case, Tabac Bar in London.

Cabify, a leading ride-hailing app in Spanish and Portuguese-speaking countries, allows users to enter 3 word addresses as destinations, so they get dropped off exactly where they want to.

KakaoMap, the main digital map provider in the Republic of Korea has also included 3 word addresses in its map natively, so people can discover, share and navigate to 3 word addresses in the app they already use every day.

Olli, an electric, autonomous bus designed by Local Motors has also integrated what3words so passengers can say 3 words to give Olli their exact drop-off point, and, speaking of electric vehicles, thousands of EV charging spots are now listed with 3 word addresses thanks to charging station-finding apps Moovility and evway.

Looking to the future of mobility

The ability to tell your car, driver and friends exactly where to go makes going places less frustrating, reduces distance travelled and time wasted, and removes the need for long calls asking for directions. This improves users’ experiences and the way they interact with a product, whether it’s a car, a delivery fleet vehicle, or an app that helps them get places.

In the fast-approaching future of autonomous vehicles, knowing exactly where you’re going and being able to communicate that information easily will become even more important. While annoying, having to explain to a driver to go a bit further and around the corner to drop you off isn’t a huge deal. But what would you do in a car with no driver to explain this to?

A 3 word address is a great way for people to communicate location simply with each other, and to tell a navigation system exactly where to go. And because they are optimised for voice, they are making navigation much easier in autonomous vehicles. The way we see it, the city of the future is 3 word addressed.

That’s why we’re not just operating in the automotive and mobility sectors. Restaurants, hotels and business all over the world now list their 3 word address in their contact details. Domino’s is delivering pizza to 3 word addresses in KSA. Lonely Planet is publishing guides with a 3 word address for every place it recommends. iStore in South Africa and Virgin Megastores in KSA now deliver goods to 3 word addresses, and postal services and logistics companies around the world have started using the system. Humanitarian aid agencies are responding to disasters and providing much-needed supplies more efficiently thanks to more accurate location information, and many emergency services around the UK now accept 3 word addresses in their control rooms, so people can say exactly where they are even if they don’t have a street address.

I’ll be giving a talk about what3words for mobility, come and see me speak at 11.50am, Tuesday 9th July.

-6uut3t.jpg)

George Hall has a background in investments and early stage start-ups. His career started in investment management, he then joined the team at onefinestay, where he was instrumental in growing the business prior to its sale to AccorHotels. Just before joining what3words, George led the growth of an e-commerce and logistics start-up from seed round to Series A. As a leader of the what3words partnerships team, George oversees all sectors with a special focus on global automotive and mobility integrations and partnerships.

There is a lot of effort being put into the development of virtual test environments for AV (Autonomous Vehicle) and ADAS (Advanced Driver-Assistance Systems). One aspect that seems to be of great interest by many is the need for high fidelity sensor models.

Many companies are currently developing sensors for autonomous driving applications and each system made available will have unique specifications and thus capabilities. To gain enough sensor measurement in the real-world in order to confirm that a given sensor meets certain requirements, will be both time consuming and expensive. The virtual environment in rFpro allows one to bypass the costs associated with purchasing equipment and acquiring a test facility whilst also incorporating real roadside factors such as the behavior of other vehicles. Simulations within this environment can be both run continuously and concurrently, which allows a large amount of test data to be acquired in a relatively short period of time. Whilst in the early stages of the development of ADAS and AV systems, it may be acceptable to utilize simple models that react and give a perfect output to the system under test; the introduction of random noise and the response to weather conditions should also be considered, both of which can improve and make the AV simulation closer to reality.

“It’s the introduction of these two characteristics that will help gain competitiveness and allow Autonomous car manufacturers to test their AI algorithms for any kind of road” says Maurizio Bevilacqua, Project Engineer at Claytex.

He continues: “To investigate this idea, we constructed a new library of Virtual Sensors for the Autonomous Vehicles Simulator rFpro”. The Library currently includes the following sensors and is being continually expanded:

Lidars

Radar

GPS

Ultrasound

Cameras

“We then simulated these sensors with different scenarios and started developing the non-idealised response that an actual sensor has” Maurizio confirms; “we have started a calibration acquisition campaign with an actual Lidar and Radar creating a database with different weather conditions, thanks to which we are able to model a coherent and realistic response to be integrated within the virtual sensors”.

ADAS systems that rely on AI devices for cognitive behavior require a large amount of training data prior to deployment and the sensor catalogue developed at Claytex can be used alongside rFpro to achieve this.

“The big challenge”, continues Maurizio, “is to define a standard and unique calibration procedure, since there is no unique standard or regulation regarding this topic”.

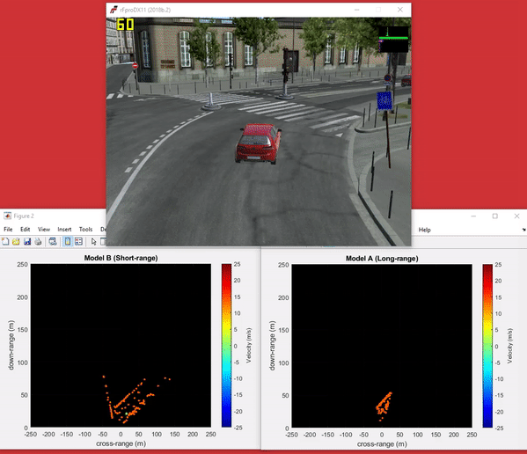

As explained before, some implementation and comparison of performance have been done as shown in the following two cases; the first one compares the performance of different radar sensors and the second one concerns the implementation of a virtual Velodyne HDL-32E.

The systems simulated here are range-doppler radars that scan in the azimuth plane. This type of sensing allows the range, angle and velocity of detected targets to be estimated and hence can be used to construct an image of the scenario being measured. The important parameters set for each device are the:

The following example uses the manufacturer specifications of three commercially available radar systems and simulates the output produced by each. One of these systems (Model C) has two modes of operation to meet the requirements of short, medium and long-range applications whereas the other two devices (Model A and Model B) operate in a single mode.

The table below shows the range, angular and frame rate parameters of the three radar systems under test:

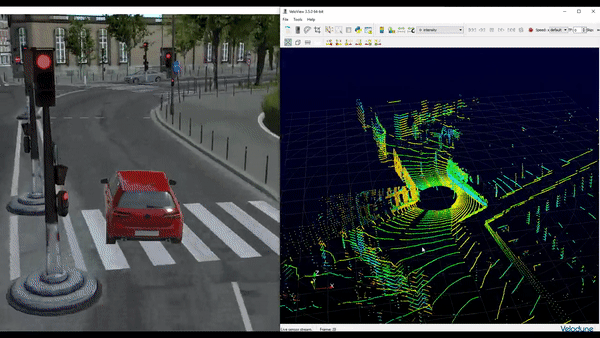

The video shows the raw output in real-time when using Model A and Model B devices on-board a moving vehicle driving around the model of Paris in rFpro.

The color of each detection within the radar plots relates to the relative velocity between the ego vehicle and the detection. Moving vehicles become distinct from stationary objects due to the doppler effect and are visible as different coloured points in the plots. Any deacceleration/acceleration of the ego vehicle will also cause the relative velocity to change.

Analyzing the performance of a cognitive system that makes use of the output produced by a set of simulated sensors will tell an ADAS system designer if the configuration under test meets the requirements set. In terms of the sensors simulated in Table 1, if the two-mode system from Manufacturer 2 is deemed adequate then a cost and packaging saving can be made. A virtual environment with accurate sensor models makes analysis of a range of sensing systems possible at a much lower cost compared to physical testing.

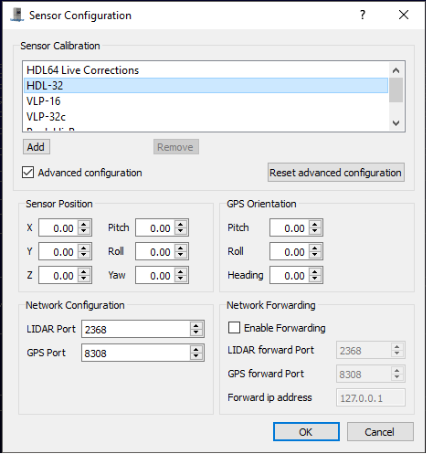

Here, it will be shown how to insert a state-of-the-art Lidar device within the virtual environment of rFpro. This will allow a user to easily stream and visualize the sensor output on any PC or storage device.

The Velodyne HDL-32E is the latest Lidar device to be added to the ever-growing database of ADAS sensors at Claytex.

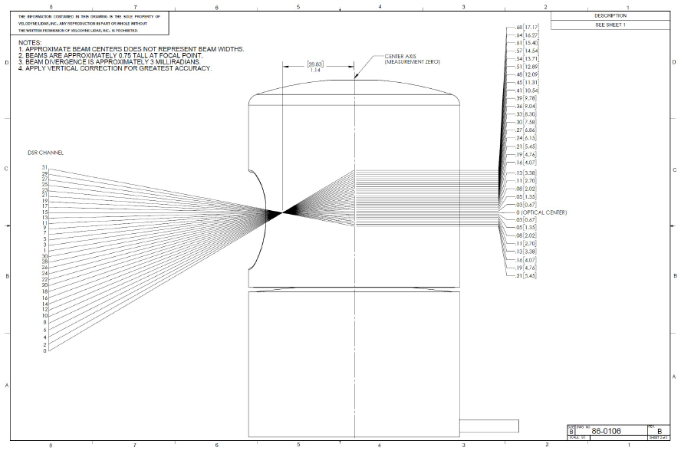

Figure 1 – Velodyne HDL-32

The Velodyne HDL-32E model uses 32 laser beams to produce an asymmetric vertical field of view (figure 2) that prioritizes the detection of ground-based objects such as pedestrians, cyclists and automobiles.

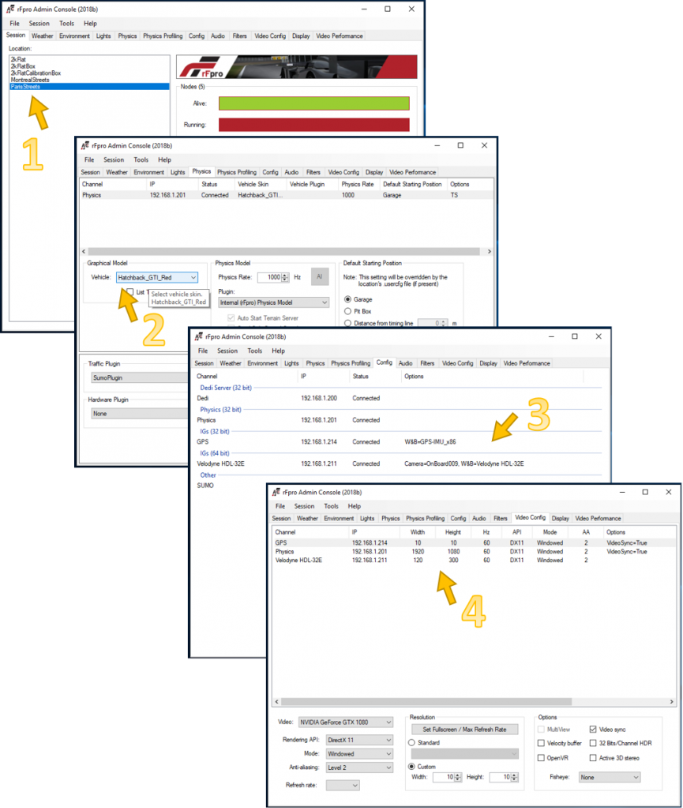

The setup procedure is simple, and it can be summarized on the following picture. Figure 3 shows the setup procedure for the ego vehicle, map and sensor.

Figure 3 – Configuration settings

The following checklist must be adhered to in the order shown:

1. The map to be used in the simulation. The simulation footage shown here was realized by selecting ‘Paris Streets’ which simulates a 2km section or road around “Les Invalides” in the 7th Arrondissement of Paris. Many real-world locations from around the globe are currently available for rFpro.

2. A car model in the Vehicles section of the Physics tab. A red hatchback was used for the results presented here. The required physics model includes the model type and the frequency of the physics model execution. The ‘Internal (rFpro) Physics Model’ was used for the results shown here with a ‘Physics Rate’ of 1 kHz but interfaces exist to all the major vehicle dynamics tools.

3. Simulation nodes must be connected and ready for execution.

4. The video settings on the Video Config tab must match the parameters of the sensor instance with the settings of the HDL-32E sensor. Also, it is important to check the video sync option is unticked; the resolution is set as 120×300 in this case.

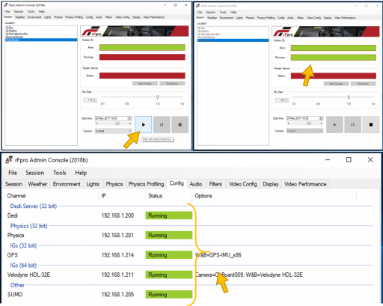

After these settings have been applied, the simulation can be started by pressing the play button in the session tab:

Figure 4 – Execution of the simulation in rFPro

The strength of this approach is that you can visualize the sensor output using the visualization software provided by Velodyne called Veloview. Veloview will not be able to tell the difference between the real and the simulated sensor outputs.

Opening Velodyne’s software Veloview and having selected the HDL-32 in the sensor calibration with the Lidar port set to 2368 (figure 5), the acquisition is ready to start.

Due to the fact that new Lidar sensors are continuously being developed to improve the capability of autonomous vehicles, new sensor models are constantly required to simulate the performance of the latest sensor configurations being considered by car manufacturers (e.g. JLR) and service providers (e.g. Uber).

“If you would like us to help you to create a customized model for a particular AV or ADAS sensor that is not currently available”, Maurizio kindly says, “please get in contact with us at Claytex, so we can help you realize such a model and thus allow you to access the benefits of simulating in a realistic virtual environment”. www.claytex.com P: +44 1926 885900

As a relatively new entrant to the autonomous vehicle industry I remember being struck how much energy we collectively spend discussing engineering aspects. Debates range from whether lidar or camera sensors are best, or who has the newest simulation technology, or how many miles research companies are going between disengagements. While this is all interesting we really need to turn our attention to what comes next and that means building businesses of sufficient scale so that we can earn back all the billions of USD / GBP that have been spent on research.

Just as Sir Tim Berners-Lee didn't invent Google, it seems unlikely that the current engineering focused companies will scale out the vehicle & mobility platforms that consumers will incorporate into their daily lives of the future. It takes a different kind of person, a different kind of business, to solve complex AI driving issues vs creating a viable consumer service at global scale.

To demonstrate the difference in thinking between engineers and consumer experience designers, look at robo-taxis, the current roll-out strategy chosen by most engineering companies with large scale autonomous vehicle plans. The concept of having an always available, cheap, consumer facing service powered by thousands of robots driving around cities looks fantastic. I can see what makes them an attractive engineering choice but as a first time consumer experience they leave a lot to be desired and as a business they are super challenging.

As a result I believe in the near term that robo-taxis are a fool's errand. Instead I propose that delivering experiences such as sightseeing via autonomous vehicle makes a better near term strategy to introduce autonomous vehicles to consumers, build trust and to create autonomous vehicle fleets that can later deliver robo-taxi services.

To explain, here are my six primary justifications:

Experiences

Can sell at the price that people pay for experiences, which is set by the market for experiences, not the market for transport. Price tends to be person, whereas taxis the price tends to be per vehicle. (e.g. a sightseeing tour can be 30-50 GBP per hour, per person)

Robot-taxis

Robo-taxi companies will be competing on price and as a result of low marginal cost, this low price is going to be incredibly low. If you are going to have immediate availability of robo-taxis (e.g. request and one arrives within minutes), you need local oversupply, creating further downward price pressure.

Summary

Following years of expensive technology investment, competing in a low price business environment seems undesirable.

Experiences

One of the great aspects of working in the experiences industry is that on occasion you deliver something amazing and it becomes a lifetime memory. This may be only 1:25 to 1:100 of purchases, but it happens.

Robo-taxis

With mobility everyone expects the core service as advertised. Anything less than that and you will have unhappy customers.

Summary

Social media will be full of people sharing their positive memories and posting photos from autonomous vehicle experiences and others ranting about why their taxi was 10 minutes late in arriving.

Robo-taxis

Customers can request to go anywhere within a region. As a result they require entire regions to be mapped. Robo-taxis compete against classic transit - if a particular junction is tricky (and has to be avoided), or in the UK you say no right turns, classic transit may turn out to be more practical for that particular routing.

Experiences

We can operate static, consistent, repeated, routes. We can design for no right turns. We can pre-map everything. We can start and end at the same location where we can have staff.

Summary

For complete rollout of autonomous vehicle experiences we only need level 4 technology. Fixed routes rather than flexible routes are easier to operate in the near term.

Experiences

When people go on a leisure trip they seek out experiences. If we can't operate at maximum scale, we descale and go upmarket if we have to.

Robo-taxis

They must become part of the fabric of a city. They must become a habit. However to create the opportunity to be habit forming, it has to be possible to take a robo-taxi whenever you want to. If you don have total scale within a city, you can't attain this habit forming level of supply.

Summary

One supported autonomous route in a city is no use for mobility, but could work for experiences.

Experiences

As we generate a reasonable minimum revenue per trip, we can do a human clean after each use.

Robot-taxis

The vehicle could finish at an inconvenient location and may have only been used for a 1km trip. If you have a fixed cleaning cost, short trips (with minimal income) may not even cover the inspection / cleaning cost. Robo-taxis have to solve the robo-cleaning problem to be viable....

Summary

Cleaning may not be top of everyone's lists of challenges but vehicle interiors are going to be public spaces. Consumers will expect them to be clean. Humans being humans, not sure this is going to be easy to do without having a human inspection after each use.

Experiences

The sightseeing industry has many incumbent companies with vehicle maintenance and operations yards, in every city in the world. Some of the largest global sightseeing companies have 3000+ buses. Vehicle maintenance and operations are part of their core businesses today.

Robo-taxis

New companies have to create new city infrastructure. This is not so easy even for companies that have existing taxi platforms as e.g. Uber / Lyft drivers live in houses, not in vehicle maintenance garages.

Summary

The bus sightseeing incumbents, although not keen on autonomous vehicles quite yet, will deliver global rollout much faster than having to start at zero with city infrastructure.

I am not a robo-taxi denier. I do believe they will come. However, autonomous vehicle sightseeing will come first, will deliver positive customer experiences & doesn't require complete city saturation to be a viable commercial service.

Convinced? Disagree? Continue the debate on twitter @alexbainbridge or contact me via email alex@autoura.com

Alex Bainbridge

CEO / CTO - Autoura

Autoura delivers vehicle based, brandable, in-destination travel experiences

@alexbainbridge

www.autoura.com

Explaining and convincing users what Mobility-as-a-Service is and why they should bother using it.

MaaS is the new paradigm of mobility, a twenty first century solution for mobility in cities. MaaS combines all modes of transport into a mobility service that could outcompete the car in terms of flexibility and affordability. It increases the customer base for all mobility service providers and incentivizes a more sustainable and active travel behavior, cities get more space for urban life and a better air quality. The story of mobility-as-a-service is impressive and the benefits endless. However the rate of expansion we are seeing today is not near the pace that was expected. Is the expansion which is happening really providing what we imagined?

The commonly acknowledged key to the success story of MaaS lies in providing an attractive offer towards travelers, but is it really enough? MaaS pioneers in Europe are currently seeing everyday public transport users quickly adopting to their services. However the usage remain much located to public transport and if the remaining benefits of MaaS are to be realised, there is one customer group that needs understand and be convinced by the offer, car owners. Without convinced car owners the sustainable city with less pollution and more urban space is difficult to realize using MaaS.

Car owners usually correspond to a financially more stable and older age group. A group who does not need and is reluctant to understand or even more so adopt anything else than car ownership. Of course a full conversion of car owners is unrealistic as the car is an important mode of transport in certain suburban areas. Nonetheless the potential difference that could be made for the mobility service provider eco system and cities remain, if urban car owners could be convinced of the potential in MaaS. The reasons why car owners are reluctant in changing is not an exact science but there are some tendencies. Car ownership is flexible mobility at a high cost. Costs which commonly are separated into different bills and difficult to overview, compiled the monthly costs reach about 616 euros[1] in average in Europe. However the cost of car ownerships often rise above the EU average in dense urban areas due to congestion charges and the cost of parking. Therefore, the fragmentation of costs, high initial investment and rapid value depreciation causes car owners to often experience both post-purchase rationalization bias and a financial lock-in effect.

UbiGo was founded out of the first MaaS service created as a pilot in Gothenburg in 2013, a pilot determined to prove the added value for all involved actors. The challenge and ultimate goal for MaaS of reaching car owners was therefore directly addressed and carefully evaluated. Resulting in more than 25% of all households were able to storage their cars and the modal distribution saw a 50% decrease in car usage in favor of public transport, biking and car sharing. This created the core of the current UbiGo concept which is currently live in Stockholm.

How can then car owners be approached? The everyday reaction and knowledge of MaaS often leave little to desire and even so often MaaS is more often associated with a river or cheese. The communication of a MaaS service is therefore key in gaining traction. With strategic, recurring and multichannel marketing we can start building an understanding for a concept commonly unheard of. Creating knowledge of what the service is instead of what is it is called. Furthermore, including the right local partners strengthens the trustworthiness. Most importantly, the main features of the UbiGo strategy involves ensuring close vicinity to high availability of station based car sharing, a special bundling of public transport tickets and a service designed for the entire household alongside a comprehensive MaaS offering. However, MaaS might be a global concept, but it is very much a local business and all new launches must be conducted carefully if the system and environmental benefits are to be gained.

Mobility as a service is a new paradigm and the twenty first century solution for mobility in cities. However MaaS needs to be implemented in a right manner incentivizing a more sustainable and active travel behavior, in order for our society to get more space for urban life and reduction of carbon emissions. Only then are we close to the realizing the true story of mobility-as-a-Service.

[1] Car Cost Index (2018). Leaseplan International

Bio - Markus Aarflot is a Business Developer at UbiGo and holds a M.Sc in Industrial and management engineering from Luleå University of Technology. He joined UbiGo as a smart mobility manager from the Swedish Transport Administration where he focused on digitalisation of ITS and bringing smart mobility to the STA.

By Sam Ryan, CEO & Co-Founder of Zeelo

We’re living in an exciting time for smart mobility. Buoyed by recent developments in transformative technologies, such as artificial intelligence (AI), the Internet of Things (IoT) and fifth-generation wireless communications (5G), the vision of fully-sophisticated smart mobility seems closer than ever. With one eye firmly fixed upon a future where every day processes and services will become increasingly interconnected, data-driven and autonomous, it’s hard not to feel a sense of excitement at the utopian ideal of a seamlessly integrated, intelligent transport network and the corollary benefits that such a system will bring – to the economy, to passenger safety, to the health and wellbeing of both people and the natural environment.

But while a future-thinking perspective is all well and good, it’s important to remember that innovation cannot be built on blue-sky thinking alone. While future smart mobility will certainly comprise an array of exciting forms of transportation – wide scale electrification of vehicle fleets, autonomous vehicles, fully-connected travel experiences and more besides – we must not lose sight of the practical steps that need to be taken in the here and now to step change transportation for tomorrow. This starts with a fundamental shift in attitudes to travel – namely, away from the singular and towards the shared.

An inconvenient truth

For close to a century, the car has been considered king when it comes to convenient transportation. In that time, demand has been both fulfilled and fuelled by ever-cheaper models produced on a hyper mass-market scale, with private car ownership per-capita rising year-on-year in virtually every nation on earth. But while current rates of ownership still far exceed the proportion of one car for every two persons across much of the developed world, a report on disruptive automotive trends from McKinsey & Company suggests the beginnings of a global downward trend in private car ownership. In the face of growing global frustration at excessive congestion on inter-city highways and in busy urban centres, and the resulting environmental concerns that such high levels of traffic bring, there is a growing acceptance that private vehicles aren’t necessarily the way that people will move in future. Some are already beginning to break the habits of a lifetime and transition towards smarter shared mobility services – though the rate at which this is happening is perhaps slower than it ought to be.

The problems faced by societies on a global scale as a result of excessive car ownership are intensifying. Congestion is getting worse, costing an estimated $305 billion in economic impact in 2017 in the U.S. alone, an increase of $10 billion from 2016. Excessive carbon emissions from traffic are polluting our air to dangerous levels, with the World Health Organisation claiming that transport accounted for almost a quarter of global carbon dioxide emissions in 2010. In addition, people are spending longer than ever commuting to and from work, regardless of how they travel, while the overwhelming need for more car parking spaces is limiting our ability to expand and grow smarter cities in the way that we want to. The fact is that while cars have long been seen as the ultimate symbols of convenience, the global overreliance on them means that these efficacy benefits are not only being outweighed by the negatives, but are simply ceasing to exist altogether. Solo travel is starting to seem less like a route to convenience and more like a roadblock.

Sharing the spoils

The idea of travelling together is certainly nothing new, but today’s innovative shared mobility services are unlike the communal travel models of old. Because of technological innovations, shared travel experiences are becoming better than ever – though this of course means that expectations are similarly increased. An influx of well-funded ride hailing startups has disrupted the transport market, while the level of on-demand expediency offered across a range of other industries has fundamentally raised the bar on what customers expect from the services they consume. People want services that are made for them, designed and developed around their wants and needs – and they not only want them immediately, but they expect them to be affordable. For the status of smart mobility to be truly accelerated, propositions must meet the skyrocketing demands that consumers have now in terms of ease and efficiency.

To do this, we can start to focus on a number of things. Firstly, transport operators and providers can invest in better onboard experiences to help solve the wellbeing and productivity challenges associated with stressful journeys. By improving communal travel experiences, whether for work or leisure, operators give people the chance of actually making the most of their travel time. Secondly, transport providers and planners must work together to bridge the current gaps in the network, as the current reliance on personal car transportation is primarily driven by a lack of genuinely compelling alternatives. Gaps in transport network can be quickly and dynamically filled by new, connected and data-driven mobility services, which are a precursor to the ultimate goal of seamlessly connected travel experiences.

Finally, and where feasible, we must look to interlink existing travel options, with a particular focus on solving the challenge of the first and last mile. If people cannot get exactly to where they need to be via shared transport, they will often begrudgingly turn back to the private vehicles they are trying to leave behind. Local municipalities and regulators have a key part to play here, as it is only by enabling the provision of data between all parties in the overall travel experience and ultimately beginning to break down the existing barriers between public and private transportation that we will start to see real progress made.

Facing the future

Improving the performance and viability of today’s shared travel options will lay a bedrock upon which to start seriously building the smarter travel networks of the future. True smart mobility isn’t here yet, and there are many hurdles to overcome as we progress towards the ultimate goal – including building the infrastructure for electric and automated vehicles, working out how these next-generation vehicles will properly interface with the human world and solving synonymous challenges in other sectors such as mobile networks. We will eventually overcome all these hurdles, and the dream will one day become reality, but hurdles do, of course, come in sequence. We cannot scale them all at once, and without overcoming the challenge of making shared mobility more attractive than solo travel, we run the risk of the remaining hurdles seeming increasingly insurmountable.

This article has kindly been contributed originally from Business Chief Europe

Graham Gordon, Director, Global Telematics at LexisNexis Risk Solutions

There are already an estimated 20 million cars in the US with connectivity capability, 11 million between UK, Germany, France, Italy and Spain and this volume is set to grow with 100% of new cars expected to have connectivity by 2025[i]. The growth in connected car data is on a steep trajectory.

Connected car data is set to change the course of motor insurance globally and the UK with Italy has a head start, leading the world in car connectivity.

Today, 10% of the UK car parc is connected. Half of this is young drivers with telematics insurance policies, with data collected through aftermarket devices. The other half is built-in connectivity in high end vehicles. By 2020[ii] all new cars in the UK are expected to be connected with the potential for data about the vehicle and how it’s driven to be used for insurance pricing and risk reduction.

Telematics insurance, a solution developed to solve young driver insurance costs is one of the first forms of connected car data and will prove fundamental to the insurance industry’s ability to meet the needs of its customer in the future.

Everything the insurance sector has learnt about risk mitigation and pricing based on real-time data will help shape the way it delivers insurance in a world where consumers will demand Usage Based Insurance (UBI) from their car.

UBI provides access to insurance priced on actual - rather than presumed - road behaviour. In the decade since telematics insurance was first introduced into the UK, claims loss ratios have reduced for insurers and premiums have come down for younger drivers. But most importantly there is now firm evidence of the efficacy of telematics insurance in reducing road risk. Our own analysis identified a 35% reduction in road casualties over the past seven years[iii] amongst 17-19-year olds as telematics adoption amongst young drivers increased[iv].

But although telematics is still very much a niche proposition, it is on the cusp of expanding to a broader market. Through the advances in technology, the cost of data acquisition has fallen by around half and there is now wider consumer appetite for UBI. Based on our research of over 3000 motorists - 60%[v] of consumers want telematics insurance.

At the same time, other types of vehicle data are now being explored, such as ADAS data to help inform insurance pricing. 60% of the UK car parc has some form of ADAS feature so this data is ubiquitous.

Fundamentally connected car data takes a variety of forms today, but the commonality is that with the right infrastructure in place it will enable the sector to deliver usage-based insurance.

Therefore, with volumes of connected car data growing exponentially, the process of gathering, normalising, understanding and utilising this data in a fully compliant manner has become a major focus for both the insurance sector and the car manufacturing markets. Both markets share a common customer and both markets want to serve that customer with mobility solutions that help improve their road safety and manage their motoring costs.

This is very much in line with the UK’s Government’s Future of Mobility Urban Strategy[vi]. This report set out nine key principles and the approach to working with innovators, companies, local authorities and other stakeholders to harness the developing benefits of new urban mobility technologies including driverless vehicles. The ninth principle states that going forward, sharing data from new mobility services - where appropriate - will improve choice and the operation of the transport system.

This will not only require collaboration, trust and consumer education, it will also put demands on mobility providers to find a way to share their data in a meaningful way and in a fully compliant manner. As the Government has stated, the principles in the Data Ethics Framework and the General Data Protection Regulation provide a starting point for this.

Insights from data can help create safer roads and support consumer choice, we have seen this in what telematics has done to cut road risk in young drivers[vii]. However, data from a wide variety of sources will need normalising to create a common understanding of mobility use to ensure these services benefit the consumer.

The challenge with connected car data is that as connected car volumes grow, there will be more and more data from many different aftermarket devices, many types of vehicles from many car manufacturers. This will demand data normalisation delivered by a neutral sever taking data from both the insurance and car manufacturing sectors. This central hub of data will help ensure consistent scoring of driving data and enable data portability, all with the consumers’ interest front and centre.

Car manufacturers are therefore looking for partnerships to help them leverage connected car data. This involves creating links with the insurance sector to help better serve their common customer. It’s already happening in the US, where major car manufacturers have joined the LexisNexis® Telematics Exchange and the first agreements in Europe are on the horizon.

Therefore, our focus right now is enabling insurance providers and car manufacturers to share data through a common platform to promote a greater understanding of risk. We see this as the starting point for the development of semi and ultimately fully autonomous vehicles.

[i] LexisNexis Risk Solutions Research of the Automotive market conducted in 2018

| 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | Avg. | 7yr CAGR (EXCEL) | Change 11 vs 17 (%) | Change 16 vs 17 (%) | |

| Total Casualties | 203,950 | 195,723 | 183,670 | 194,477 | 186,189 | 181,384 | 170,993 | 188,055 | -2.49% | -16.15 | -5.73% |

| 17-19 | 18,529 | 16,620 | 14,261 | 14,715 | 13,774 | 12,772 | 11,984 | 15,112 | -6.04% | -35.32 | -6.17% |

| 16-24 | 49,364 | 46,530 | 41,388 | 42,862 | 40,576 | 37,979 | 34,951 | 41,950 | -4.81% | -29.19 | -7.97% |

| 25-59 | 107,573 | 105,382 | 100,762 | 107,270 | 103,120 | 92,101 | 95,732 | 101,706 | -1.65% | -11.00 | 3.94% |

| 60+ | 23,979 | 23,357 | 22,712 | 24,544 | 23,369 | 23,409 | 22,375 | 23,392 | -0.98% | -6.68 | -4.42% |

| Total 16-to 60+ | 153,058 | ||||||||||

| Total under 16 | 17,935 | ||||||||||

| Total Casualties | 170,993 |

[iv] 975,000 live policies, over 1m 17-19-year-old drivers - https://www.biba.org.uk/press-releases/biba-research-reveals-telematics-almost-reach-one-million-mark/

[v] Consumer Intelligence Research conducted September 2017 of 3025 motor insurance policyholders. Respondents were 50% males, 50% females and representative of the driving population across 7 age groups (17-19, 20-24, 25-34, 35-44, 45-54, 55-64, 65+) and social demographic groups –A, B, C1, C2, D, E.

| Classification | Description | Percentage of Population | Survey Respondents |

| AB | Higher & intermediate managerial, administrative, professional occupations | 22% | 38% |

| C1 | Supervisory, clerical & junior managerial, administrative, professional occupations | 31% | 32% |

| C2 | Skilled manual occupations | 21% | 16% |

| DE | Semi-skilled & unskilled manual occupations, Unemployed and lowest grade occupations | 26% | 15% |

[vi] https://www.gov.uk/government/speeches/future-of-mobility-urban-strategy

[vii] https://risk.lexisnexis.co.uk/about-us/press-room/press-release/20181114-young-driver

New mobility trends, such as ride-hailing and vehicle electrification, are driving improved transportation cost structures and have the potential to bring significant opportunity to the value chains of many businesses. With the right approach, businesses across the economy can see mobility as a stimulus for business model innovation, creating new revenue opportunities and improving operating efficiency.

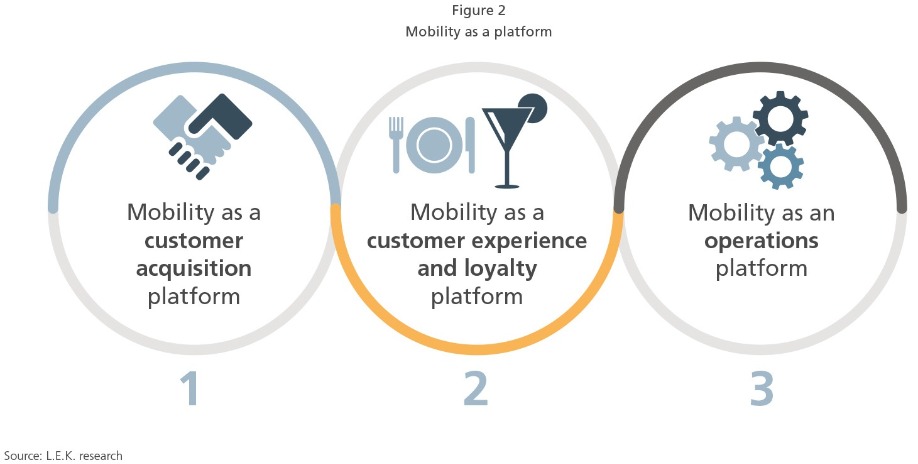

L.E.K. Consulting’s framework — ‘mobility as a platform’ (MaaP) — provides a lens through which businesses can consider options for growth, through customer acquisition, customer experience and loyalty, and business operations.

Bending the cost curve — road transport trends

MaaP is enabled by significant improvements in the cost structure of transportation, underpinned by two key new mobility drivers:

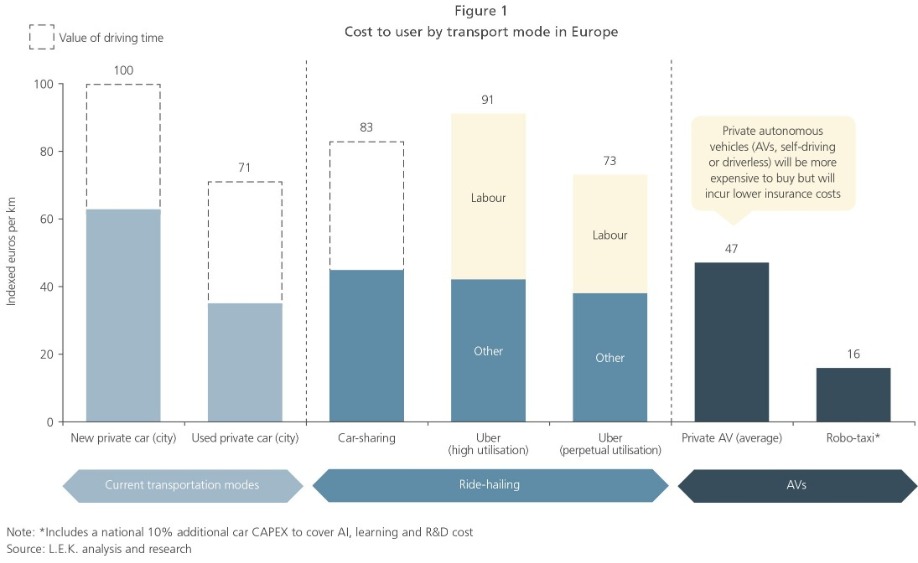

1. Sharing and autonomy (in urban contexts). The mission statement of shared mobility disruptors (Uber, Lyft, Zipcar, etc.), and indeed the strategy of some OEMs reacting to these trends, is to displace car ownership. This seeks to effectively monetise the 95% of unused capacity that consumers pay for when they buy — but don’t use — a car. Improved utilisation, custom vehicles and eventually autonomous driving will change the cost such that a consumer could get on-demand transport at a more favourable cost point than owning a vehicle (see Figure 1).

2. Vehicle electrification. The transition from fossil fuels into alternatively fuelled vehicles — in particular electricity — could drastically reduce fuel costs. U.K. businesses and consumers currently spend about £50 billion on diesel and petrol every year; the equivalent in the U.S. is about $530 billion (or $4,200 in ultimate costs borne per household, on average). As electric vehicle ‘total cost of ownership’ economics approach parity with internal combustion engine vehicles, the transition to electricity will accelerate and could materially reduce costs related to transportation fuel.

As transportation costs deflate, the key question is how the value chains of other industries are impacted and what business opportunities emerge. For example, the democratisation of air travel created a number of beneficiaries, including destination holiday resorts, which acquired a new and vastly enlarged cohort of customers. More latterly, new business models have emerged for everything from innovative accommodation providers (e.g., Airbnb) and traveller advice services (e.g., TripAdvisor) to aggregators that stitch the travel value chain together (e.g., Expedia). And let’s not forget consumers, who have made significant savings and gained a richer experience along the way.

While it is still early days for urban transportation, there are parallels from these industries that point to innovation opportunities for all companies relying on transportation.

MaaP – L.E.K.’s framework for mobility-inspired innovation

L.E.K.’s MaaP framework allows organisations to identify opportunities for business model innovation, leveraging new mobility services and their associated lower transportation costs (see Figure 2).

Figure 2 — Mobility as a platform

I. Mobility as a customer acquisition platform

As sharing, automation and electrification dramatically reduce transport costs per mile, their reach amongst consumers is expected to improve. Mobility platforms already touch a large proportion of consumers in big cities; over 3 (out of 9) million Londoners have used a ride-hailing service, and more than 30 million North American riders used Lyft services in 2018. In a short period, mobility platforms have already created a new means of accessing a large, addressable customer base.

Take for instance Cargo, a startup that provides free goods (from items of confectionery to electronics) to rideshare drivers to market and sell to passengers. Through its global collaboration with Uber, Cargo is hoping to target a captive audience that has disposable income and a willingness to experiment. Consumer brands are also having their products sampled or purchased in a new and relevant channel, bypassing traditional convenience retail channels and creating a data-rich interaction with end customers; it also improves driver earnings, creating a win-win situation.

As a general point, there are a large number of high fixed-cost industries whose economics could benefit from even a modest increase in utilisation. An empty cinema complex on a weekday afternoon, a restaurant chain in the business district on weekends, a theme park with idle capacity outside of school holiday periods — all are examples where funding the ‘customer acquisition cost’ of a mobility fare to/from the venue could markedly improve business performance.

II. Mobility as a customer experience and loyalty platform

Propositions leveraging mobility to enhance the customer experience can create powerful economics for businesses and, in turn, improve customer value and loyalty.

For example, Tesco, one of the leading supermarket operators in the U.K., recently launched an initiative to install 2,400 EV charging stations across 600 sites, with a promise of ‘free’ trickle charging and paid upgrades to fast charging. On a stand-alone basis, the ability to break even on large charging infrastructure is unlikely to be possible for some time. However, when considering system economics — becoming the shopping destination of choice for EV owners (thus improving the customer experience and loyalty), and increasing dwell times while waiting for adequate charge to be achieved — the trade-off becomes more compelling, with potential for both customer volume increases and like-for-like shopping basket growth.

Where shopping baskets are of a sufficient value, a paid enhancement to the customer experience can help improve overall revenues by stimulating volumes and market share gains. Enterprise famously created the “We’ll pick you up” promise, which helped cement its position in off-airport car rental locations. However, the concept was not without friction — in part due to the need to make calls at least two hours in advance. On-demand mobility changes this paradigm. ViaForBusiness or Uber4Business are already creating the functionality for businesses to support their customers by integrating mobility services.

III. Mobility as an operations platform

Perhaps the most straightforward opportunity is the rewiring of operations to benefit from developments in new mobility. Diageo, the international beverage manufacturer, has partnered with Deliveroo and UberEats to deliver alcoholic beverages to consumers in homes on an on-demand basis. This new experimental channel is allowing a traditionally B2B2C company to increase its B2C presence, enabled by last-mile mobility. From a system perspective, bypassing the traditional distribution channels saves significant distribution cost while also reducing pricing pressure that is typically present in FMCG-retailer negotiations.

There are likely to be a number of use cases for on-demand mobility as a logistics application, where either part or the entirety of fleet requirements for a distribution venture could be served by more appropriate on-demand modes in a cost-effective (and a potentially carbon-effective) manner.

Economic and social benefits

The opportunities of MaaP are plentiful. Alongside being used as a platform for customer acquisition, customer experience and loyalty, and business operations, MaaP may also enable the corporate social responsibility agenda for large corporates. As carbon footprints, air quality and plastics consumption continue to be hot topics, the transition to electric, shared and on-demand mobility could dramatically change the economics of closed-loop supply chains. Furthermore, the landscape is ripe for mobility to be used as an accessibility platform, helping provide the elderly or infirm access to wider services to improve quality of life, or improving accessibility for disabled persons to become more actively involved in the workforce.

L.E.K.’s MaaP framework demonstrates the scope of opportunity available. Now it is time for businesses to consider how they can innovate, using these newly emerging mobility services and trends as a backbone for future growth.

Ashish Khanna is a Partner at L.E.K. Consulting, a global management consulting firm. He is the co-leader of L.E.K.’s global New Mobility practice and is an active commentator on the trajectory of transportation technology innovation across connectivity, sustainability and automation. He has been at the forefront in advising governments, infrastructure investors and businesses globally on the potential impact and opportunities arising from new mobility trends. Ashish holds an MBA with Distinction from INSEAD.

L.E.K. Consulting is a global management consulting firm that uses deep industry expertise and rigorous analysis to help business leaders achieve practical results with real impact. We are uncompromising in our approach to helping clients consistently make better decisions, deliver improved business performance, and create greater shareholder returns.

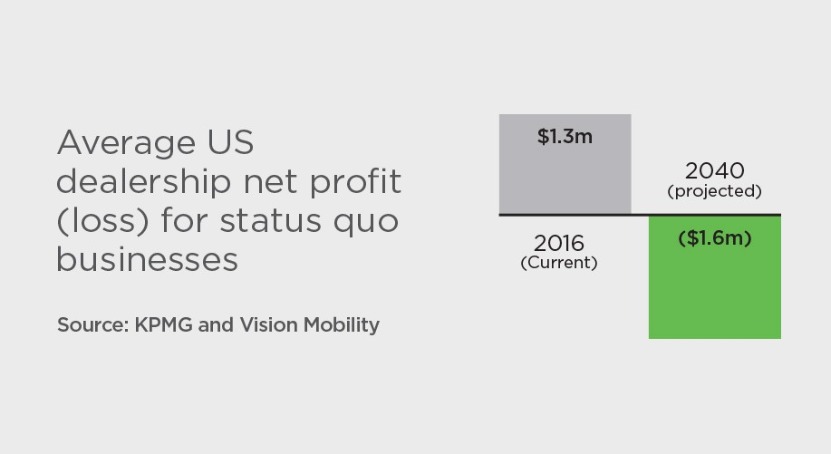

No one can doubt that the last 100 plus years has been kind to automotive retail. It has allowed ordinary people to develop a profitable business, and with appropriate management, one with longevity such that many businesses have been passed down through multiple generations. It has made some owners very wealthy indeed.

As car technology has improved and vehicle sales and servicing techniques refined, the concept of buying a wholesaled vehicle from an OEM and retailing it to a customer has changed surprisingly little. Even with the advent of the internet, the sales process remains remarkably similar to 30 years ago for most dealerships.

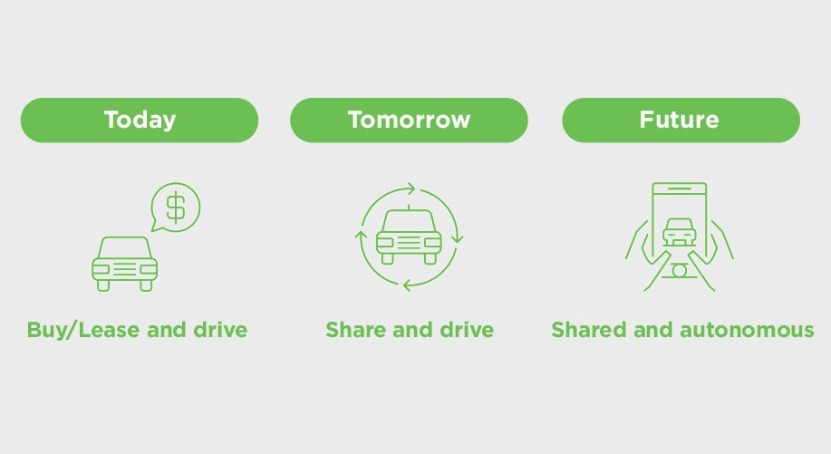

The introduction of Shared Mobility, and the future possibilities it brings, has the potential to bring some dramatic changes to this tried and true business model. Technology is certainly one driver for this potential change. Vehicle connectivity, autonomous driving, Shared mobility business models and electric vehicles, are coming together to bring all the ingredients needed to disrupt vehicle ownership. Additionally, there is an emerging change in attitudes regarding car ownership. Together, technology changes combine with societal changes have the potential to offer an alternative to the traditional dealer poor customer experience and expense of car ownership.

Most thought leaders in Shared Mobility cite a utopia of extremely low cost, fleet operated, on demand “Taxi Bots”, or autonomous Ubers, that pick people up and take them wherever they want to go, all for a small fraction of today’s ownership costs. This model creates the same convenience of today’s vehicle ownership, but with a much smaller impact on a household’s budget.

Love to drive or love to own: Shared Mobility brings low cost alternatives

While many dealers will cite a customer’s attachment to their vehicle and a desire to own as reasons for very limited change. However, research in the Annual Mobility Study has found that while more than 70% of people enjoy driving, fully 35% of respondents said that they would not own a car if they didn’t have to. Clearly love to drive and love to own aren’t the same thing or everyone.

The survey also found that Gen Z and millennials were also the least likely to enjoy driving, and the most likely to not own a vehicle if they didn’t have to. This generational shift in attitudes is also reflected in other ways, such as less likely to obtain a driver’s licence in their teen years, and more likely to spend money on experiences than purchases of vehicles or other expensive items.

This generation also places greater value on causal issues such as pollution and congestion reduction, equity and social justice; all issues that that can potentially be addressed through Shared Mobility transportation offerings.

To put it succinctly, Shared Mobility brings low cost alternatives to car ownership, and offers it to a generation who are much more likely to see the value in such a change.

Let’s take a closer look to see how dealers will fair in a Shared Mobility retail environment by examining their business through the SWOT business analysis model.

Timing is everything: Plan ahead for the on-demand revolution

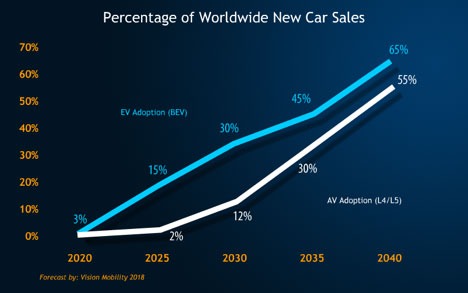

By 2030, Vision Mobility forecasts that 30% of all new vehicle sales will be battery electric, while 12% will have ‘full’ Level 4/5 Autonomous capabilities. This means that while dealers do have time to determine a way forward and begin putting in place measures that will generate success in a Shared Mobility environment, there is significant urgency if a dealer wants to be on the forefront of change.

The obvious alternative to not being on the forefront of change is obsolescence through industry disruption, and we can site any number of companies and industries that were not able to make the breakthrough. CDs, film photography, DVD video rental – all relics of another age.

A clear path forward

The good news is that dealers can take advantage of their strengths and incumbent status to make the most of opportunities that Shared Mobility has to offer. Utilising a Car as a Service platform, like that provided by Ridecell to many different car sharing and micro-mobility operators, dealers can attract short-term usage customers who they have never seen before, some of whom will be in a position to buy soon after using the vehicle. Customers may also be retained when their life circumstances change, allowing their previous vehicle to be sold and a short-term vehicle used as needed. It also allows dealers to plan extended test drives and thereby maintain a relationship with a customer who does not purchase.

We’ve noticed in our own discussions with dealers that once the idea of CaaS is understood, dealers are able to quickly apply the concept to new opportunities in their own local trade area. Such ideas we’ve heard include providing shared vehicles for Uber and Lyft drivers, using low cost shared vehicles for low income families, targeting one off usage with pickup trucks, vans and luxury cars, and supporting local charities through low cost vehicle usage sponsorship.

A Car as a Service platform also has the advantage of improving demo and shuttle utilization, and improving inventory management by allow a rotation of vehicles on and off the CaaS program at the most opportune time. This results in improved usage efficiency of the vehicles on the ground, that not only generates significant cost savings over time, it allows the vehicles to generate revenue when they would otherwise just be sitting around.

However, it is how dealers can position themselves for Shared Mobility that we believe is the most valuable. Most experts believe that future mobility will heavily utilise low cost fleet operated taxi bots (autonomous Uber), and these vehicles must be operated by a Car as a Service platform, thereby creating a direct link to the future. In the meantime, the platform allows dealers to sharpen their fleet management skills and streamline their fixed operations side to accommodate such a program.

In summary, very significant change is coming to retail automotive over the next 10-15 years on a scale that has never been seen in its 100 year history. In order to survive and thrive, dealers must start taking active steps today to understand the coming impact of Shared Mobility and adopt new business strategies that will allow continued success for the future. The Car as a Service platform opens up many new possibilities today that compliments a dealer’s traditional activities, as well as positioning the dealership for a successful and prosperous future.

James Carter is Principal Consultant of Vision Mobility, and well known for his activities and thought leading discussion on the automotive and mobility retail environment in Shared Mobility. Prior to founding Vision Mobility, James spent 19 years with Toyota in Australia, Japan and North America in a variety of sales, marketing, strategy and operations roles, and has significant experience with dealership activities and process.

Mark Thomas is the VP of Marketing and Alliances at Ridecell and is responsible for marketing Ridecell, the world’s leading platform to build, operate and scale new car and ride sharing mobility services. Prior to joining Ridecell, Thomas headed the connected car marketing team at Cisco Jasper, where he developed the product and go-to-market strategies for automotive OEMs. Prior to Cisco, Mark led product marketing at HERE, a leading automotive maps company. In addition, Mark served in marketing, strategy, and business development roles at Apple and Nokia. Mark holds a B.A. from University of California, Berkeley, and an M.B.A. from the University of Pennsylvania Wharton School of Business.

Photo by Zach Inglis on Unsplash

2012 was a breakthrough year for car clubs in the UK, with rapidly growing member numbers, high profile acquisitions and new entrants to the market, so much optimism surrounded the nascent industry that it was predicted at the time that there would be a million subscribers by 2020. In fact, in 2017 the total UK fleet was only 4000 vehicles* and while member numbers continue to grow, 85% are concentrated in London which only had 193,500*. For context in that time 680,000 more vehicles per year have been added to UK roads**.

So where are all the shared cars?

If you live in a city like London, you have access to a world class public transport system - you can chose underground trains, over-ground trains, buses and even boats; you also have the traditional black cab, a plethora of ride hail apps, docked bikes, dockless bikes and probably in the next few months e-scooters as well. On the rare occasions only a car will do, there are a number of car share clubs.

If you live in a town or village you probably have access to a public transport network (possibly an infrequent one) and a couple of the other services listed above such as a minicab service - but you are unlikely to be able to access a shared vehicle on a flexible hourly basis from a car club.

The rationale is simple: it’s a terrible idea to own a car in an urban environment, so even though city dwellers are better served with mobility options than anyone else, and rarely need a car to travel, car clubs operate in these markets to fulfil this occasional demand.

But is owning a car outside a city, say in a small town such a good idea either?

Cars are expensive to own and maintain, though given the damage they are causing to the environment and people’s health they should probably cost considerably more, they are parked 95% of the time and on the rare occasions they are used despite having 5 or more seats, most of the time they are only occupied by 1 person.

Shared vehicles, especially when combined with shared rides, seem an obvious answer especially for communities that lack other options. So why isn’t there a shared car on every street up and down the country?

The answer is simple - risk.

Risky business

In fact, it’s the dual risk of taking on a high fixed cost for a vehicle, probably on a 2 or 3 year lease, and the risk that when it is in situ not enough people will use it.

With these two factors it becomes hard to make a business case to spread the undeniable benefits of access to shared vehicles beyond the biggest cities - so no one does. A solution which potentially offers communities in towns and villages the greatest benefits is never even offered to them.

The problem is that car sharing organisations continue to approach these risks from a traditional asset owning point of view, where service providers must also be asset owners. That seems at odds with other modern businesses, for example Uber (one of the largest taxi services in the world doesn’t own any cars) and AirBnB (the accommodation provider with no property) are frequently used retorts to that traditional model but are far from the only precedents. Businesses the world over no longer buy outright, or develop their own software applications, instead they use low cost, flexible Software-as-a-Service models and pay based on their usage.